The UV curing system market is growing at a pace that cuts across nearly every industrial sector. Multiple research firms project substantial expansion through 2032 and beyond, driven by the convergence of tighter environmental regulations, automation investment, and the rapid maturation of UV LED technology. Understanding these dynamics helps manufacturers make sharper equipment and capital decisions before competitors do.

This article breaks down the current market size and share data, the five trends reshaping adoption, what's driving growth, and what signals point to where the market is heading next.

Key Takeaways

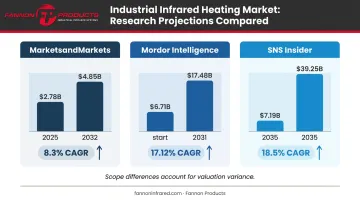

- The global UV curing system market is valued at $2.78B–$7.19B in 2025, with projected CAGRs of 8.3%–18.5% through 2032–2035

- UV LED technology is the strategic growth direction, with energy savings of up to 80% lower power consumption versus conventional UV lamp systems

- Asia Pacific holds 41.88% of 2025 market value and is forecast to grow at the highest regional CAGR of 10%

- VOC limits and mercury-phase-out pressure are making UV LED adoption a compliance issue, not just a cost decision

- Adhesives, printing, and electronics assembly are the largest and fastest-growing application areas

UV Curing System Market Size and Share: What the Numbers Say

Market sizing for UV curing systems varies significantly depending on which research firm you consult — and the scope differences matter.

| Source | 2025 Market Size | Projected Size | CAGR |

|---|---|---|---|

| MarketsandMarkets | $2.78 billion | $4.85 billion (2032) | 8.3% |

| Mordor Intelligence | $6.71 billion | $17.48 billion (2031) | 17.12% |

| SNS Insider | $7.19 billion | $39.25 billion (2035) | 18.5% |

These divergences reflect different scope definitions, not data errors. Some reports include adjacent chemistry markets; others focus strictly on curing equipment. Across all three sources, the direction is the same: a large market growing at a strong clip.

How the Market Breaks Down

By technology:

- UV LED systems: largest segment by new system selection (MarketsandMarkets, SNS Insider)

- Mercury vapor lamp systems: still 52.42% of 2025 revenue by installed base (Mordor Intelligence) — a figure that reflects legacy systems, not new purchases

- Hybrid LED/arc systems: emerging bridge technology for mixed-substrate operations

By system type:

- Conveyor/inline systems: 38–52% of demand depending on source — the dominant configuration for high-volume production

- Spot cure systems: largest segment per MarketsandMarkets for precision bonding applications

- Flood systems: used for wide-area coating cure

By application:

- Printing: 35–60% of revenue depending on scope

- Adhesives/bonding: largest application per MarketsandMarkets; critical for electronics and automotive assembly

- Coatings, 3D printing, and medical device assembly: fast-growing secondary segments

Regional Breakdown

Mordor Intelligence reports Asia Pacific held 41.88% of 2025 market value, while SNS Insider places North America at approximately 36%. Europe's verified share wasn't available in authoritative public sources. Manufacturers should not rely on inferred figures for strategic planning.

5 Key Trends Reshaping the UV Curing System Market

Trend 1: Rapid Shift to UV LED Technology

UV LED curing has become the default choice for new system installations — and the reasons go well beyond environmental branding.

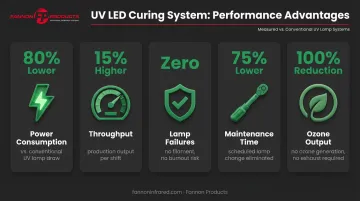

The practical advantages are measurable. A Flexographic Technical Association case study on UV LED flexo packaging found:

- 80% lower power consumption vs. conventional systems

- 15% higher throughput

- Zero lamp failures over the study period

- 75% lower maintenance time

- 100% ozone reduction

In label converting, GEW reports that one converter avoided a $150,000 power-grid upgrade after retrofitting with UV LED — a hard financial justification that procurement teams can take directly to capital budget reviews.

Key technical advantages driving adoption:

- Instant on/off — no warm-up time, no idle energy burn

- Precise wavelength control — critical for sensitive substrates in electronics and medical assembly

- Lower heat output — essential for films, plastics, and heat-sensitive inks

- No ozone generation — eliminates ventilation infrastructure costs

Fannon Products manufactures purpose-built UV LED curing systems at their Michigan facility, designed specifically for inkjet and screen printing applications. Their three-module lineup (3-inch, 6-inch, and 9-inch) operates at 395–405nm with a consistent 16 W/cm² power intensity across all models — a specification that supports predictable curing across production line widths without overpowering the substrate.

Trend 2: Integration with Automation and Industry 4.0

UV curing systems are increasingly embedded into automated production lines rather than operating as standalone units. Real-time UV intensity monitoring, transport interlocks, and process-parameter tracking allow manufacturers to maintain curing consistency at high line speeds without manual intervention.

Companies like Hönle document UV Cell process monitoring systems that track irradiance and operational parameters throughout the curing line. UPRtek's semiconductor UV measurement documentation illustrates how process insights feed back into quality control workflows for precision applications.

What this means for manufacturing operations:

- UV systems that communicate with line control systems (via dry contact or 24 VDC interfaces) enable synchronized start/stop with substrate movement

- Real-time monitoring reduces reject rates tied to under- or over-curing

- IoT-enabled process data supports predictive maintenance without waiting for system failure

Fannon's UV LED systems include built-in transport interlocks as standard — a foundational integration feature that connects curing operation to broader line control without custom engineering.

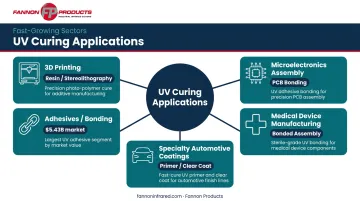

Trend 3: Expansion into Emerging Application Areas

UV curing demand has expanded well beyond printing and coatings. Several high-value sectors are pulling significant new volume.

Adhesives are among the largest application segments by market value. Mordor Intelligence values the UV-curable adhesives market at $5.43 billion in 2026, growing to $7.09 billion by 2031 at a 5.48% CAGR — driven by the need to bond dissimilar materials (plastics to metals) rapidly in automotive and electronics assembly.

Other fast-growing application pockets include:

- 3D printing — resin curing for stereolithography and photopolymer inkjet (NIST roadmap confirms scale-up trajectory)

- Microelectronics assembly — UV adhesive curing for component bonding on PCBs

- Medical device manufacturing — UV-cured adhesives used in nearly all bonded device assemblies

- Specialty automotive coatings — primer, clear coat, and powder coat applications

Trend 4: Environmental Regulations Accelerating Mercury Phase-Out

Regulatory pressure on mercury use and VOC emissions is functioning as a structural demand driver — not a future risk, but a present-tense operational reality.

Conventional UV curing lamps contain 10–100 mg of elemental mercury per lamp, according to GEW. While the Minamata Convention does not currently mandate an outright ban on industrial mercury vapor lamps, the regulatory trajectory creates real compliance risk for facilities running legacy systems.

The EU's Industrial Emissions Directive (2010/75/EU) sets VOC waste-gas limits — heatset web offset printing above 15 tonnes/year solvent consumption carries a 100 mg C/Nm³ limit. US EPA guidance similarly pushes facilities toward low- or no-VOC ink and coating formulations.

UV LED systems address these pressures directly:

- Solvent-free cure chemistry eliminates VOC emissions at the source

- 100% ozone reduction eliminates ventilation infrastructure requirements

- No mercury content removes end-of-life hazardous material disposal

- Lower energy draw supports ESG reporting and carbon reduction commitments

For manufacturers with ESG disclosure requirements, UV LED adoption checks compliance, cost, and sustainability boxes simultaneously.

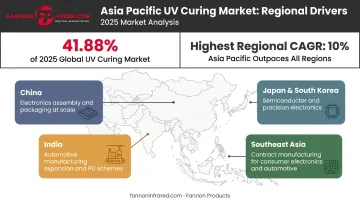

Trend 5: Asia Pacific's Rise as the Dominant Growth Region

Asia Pacific holds 41.88% of 2025 global UV curing market value — making it already the largest regional market, not merely the fastest growing. MarketsandMarkets projects it will register the highest CAGR at 10.0% through the forecast period, outpacing both North America and Europe.

The volume is concentrated in specific manufacturing hubs:

- China — electronics assembly and packaging manufacturing at massive scale

- India — automotive manufacturing expansion, supported by production-linked incentive schemes for advanced automotive technology

- Japan and South Korea — semiconductor and precision electronics production

- Southeast Asia — contract manufacturing for global brands across consumer electronics and automotive components

The combination of manufacturing density, automation investment, and tightening environmental standards across the region creates compounding demand. Fannon Products ships factory-direct from their Michigan facility with 99% secure delivery globally — reaching this demand without requiring regional manufacturing infrastructure.

What's Driving These UV Curing Market Trends

UV curing adoption isn't a single-driver story. Technology, cost economics, compliance pressure, and competitive dynamics are all moving in the same direction — and reinforcing each other.

Technology: LED efficiency improvements, hybrid curing platform development, and digital control systems have expanded what UV curing can do. Component-level innovation is visible in recent product launches — including ams-OSRAM's OSLON UV 3535 (October 2024) and Luminus's SST-08-UV high-power UV-A LEDs in 365–405nm wavelengths (May 2024) — advancing output power and wavelength precision with each product cycle.

Cost economics: High-speed production lines and just-in-time manufacturing demand fast cycle times. UV curing delivers instant cure versus extended dwell times in thermal ovens — RadTech confirms that UV processes typically increase production rates and reduce scrap. As LED system costs decline, the total cost of ownership calculation shifts further in UV's favor over thermal alternatives.

Compliance pressure: VOC standards, mercury restrictions, and energy mandates across North America, the EU, and parts of Asia are non-discretionary. Facilities running legacy solvent-based or mercury lamp systems face an upgrade timeline driven by regulation — not preference.

Competitive dynamics: Intensifying competition among UV curing system manufacturers has pushed prices down and product specs up, opening the technology to small and mid-sized manufacturers that previously found it cost-prohibitive. For industrial suppliers, this creates a long-term revenue model built on replacement components and system upgrades — not just equipment sales. Fannon Products operates exactly in this space, offering UV LED curing systems alongside direct-replacement lamp and component supply for existing lines.

Future Signals for the UV Curing System Market

Three developments are worth monitoring over the next 1–3 years:

1. UV curing in additive manufacturing scale-up NIST's photopolymer additive manufacturing roadmap covers stereolithography, inkjet, and photopolymer-based 3D printing at industrial scale. As AM moves from prototyping to production, UV curing system demand follows.

2. AI-driven curing optimization and IIoT integration IIoT-enabled predictive maintenance is moving from pilot to production — monitoring irradiance, dose, and process consistency in real time to flag maintenance needs before failures occur. Systems with open sensor interfaces are increasingly positioned to support this integration without additional retrofit work.

3. Hybrid mercury/LED systems as bridge technology For converters running mixed ink and substrate portfolios, hybrid LED/arc systems allow job-by-job switching between curing sources. Industry analysts note this as a practical transition strategy for facilities that can't immediately standardize on UV LED chemistry.

Scenario outlook for 2025–2027:

- Continued LED price compression lowers adoption barriers for SMEs

- Regulatory tightening in Asia Pacific accelerates mercury lamp retirement

- IIoT infrastructure buildouts are pushing sensor-integrated, fully automated UV curing lines toward the production standard in high-volume operations

Frequently Asked Questions

What is the current size of the UV curing system market?

Market size estimates range from $2.78 billion to $7.19 billion in 2025, depending on research firm scope. Projections through 2032–2035 range from $4.85 billion (MarketsandMarkets at 8.3% CAGR) to $39.25 billion (SNS Insider at 18.5% CAGR). Use source-specific figures rather than averaging across reports.

What is driving growth in the UV curing system market?

The primary drivers are rising demand for fast, eco-friendly curing, automation adoption in smart manufacturing, VOC and mercury regulations, and expanding applications in electronics, automotive, and packaging.

What is the difference between UV LED and mercury lamp curing systems?

UV LED systems offer greater energy efficiency, longer operational lifespan, instant on/off capability, and lower heat output. Mercury lamps have a larger installed base and lower upfront cost but carry mercury content, require ozone ventilation, and face growing regulatory pressure — making LED the clear direction for new installations.

Which industries use UV curing systems the most?

Printing and packaging, automotive coatings, electronics assembly, medical device manufacturing, and industrial adhesives are the leading industries. Application leadership varies by source: MarketsandMarkets ranks adhesives/bonding first, while Mordor and SNS Insider data show printing leading by revenue share.

Which region is growing fastest in the UV curing system market?

Asia Pacific is the fastest-growing region, already holding 41.88% of 2025 market value and projected to register the highest regional CAGR of 10% through the forecast period. Growth is concentrated in China, India, Japan, and South Korea.

Are UV curing systems environmentally friendly?

UV curing is substantially more eco-friendly than thermal or solvent-based alternatives — it's solvent-free, produces lower VOC emissions, and consumes less energy. UV LED systems go further by eliminating mercury content entirely and generating zero ozone, making them the preferred choice for facilities with ESG and emissions compliance requirements.